November was another difficult month in the market. The 4th quarter has wiped out all of our gains for the year. After meeting with our financial planner, we are harvesting some capital losses to help improve our tax situation. It amazes me that our asset portfolio is getting to the point where we can make adjustments that impact our tax situation.

I’m still finding my footing with the new job. In exchange for the pay raise, it consumes more of my time. We went into the change with open eyes and made the decision partly based on the positive impact to our financial independence timeline, understanding that it would negatively impact my free time in the short term.

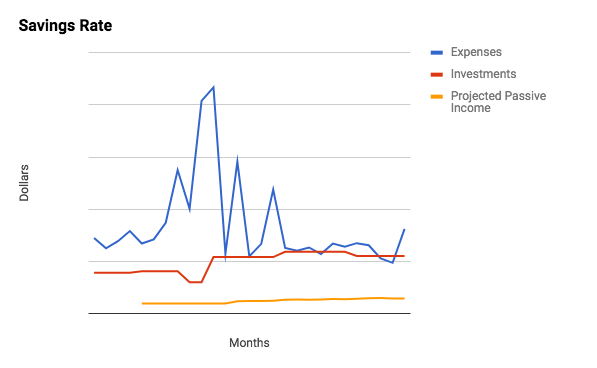

November was our highest spending month of the year and December will probably be even higher. We made a deposit on a home improvement purchase in November–which was the biggest component of our spending spike. Our restaurant spending was high in November, too. We traveled to a destination half marathon for me and the friends we visited planned several pricey restaurant excursions. Our timeline, budget, and current earning can absorb these kinds of occasional treats. The key is to make sure they don’t become habits. We have been tracking our spending for over a year now and comparing the data is so interesting. As we near the end of 2018, we can see how much progress we made in reducing our spending. Our priority is always how to have more fun with fewer dollars.

We’ve made plans to significantly increase our investment contributions based on my new salary and paying off our car loan. Automating our savings is the most, and for us possibly the only, effective way to reach our goals.

With that, how did we do on our November goals?

- Total spending within budget

- D As I mentioned, November was our highest spend month. But subtract out the home improvement item and we were pretty close to budget.

- Finish reading current Kindle book (Ms. Vine)

- A Yes! I finally finished reading Shogun

- Finish previously planned destination half marathon (Ms. Vine, despite breaking my foot)

- A I finished this half marathon, which was one of the most mentally difficult races I’ve completed. I managed this race using a run-walk interval method.

- Publish one blog post in addition to monthly update

- F This didn’t happen, despite my best intentions

- Pre-pay 2018 estimated tax bill

- F This also didn’t happen, but we might take care of it in December

- Schedule increased investment contribution with financial planner

- A We completed this

- Set up new 401k for management by financial planner

- A This is also complete

I don’t even want to set any goals for December. Maybe just “survive until the end of the year”. We’ve got some big things and another trip coming up this month. With the hectic end of the year, we’ll focus on more wellness related goals for December:

- Publish one blog post in addition to monthly update

- Daily exercise (we’re reviving this one now that my foot is sufficiently healed)

- Restaurant and grocery spend within budget

- Complete one item from 101 things list

Yikes at the blue line spike! But I am happy to see that (1) it’s a spike and (2) even this jump is below our spending for much of 2017.

As a reminder, our goal is to reach financial independence (which we define as no longer needing to work to pay our bills). Our nest egg goal is lower than what our financial planner recommends, but is based on our current expenses, less a 0% interest car loan that will be paid off in January 2019. We did not strictly follow the 4% rule (Trinity Study). Our mortgage is currently scheduled for payoff in 2029 and we don’t expect to do so before reaching financial independence. Of course, this is subject to change, but the payment and interest rate are quite low. We plan to keep travel and other discretionary spending low if decide to retire early while we owe a balance on the mortgage.

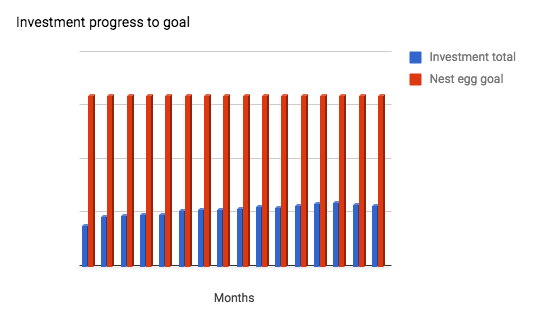

The rough market resulted in a drop in the investment:nest egg ratio, despite making our regular contributions.

One Comment